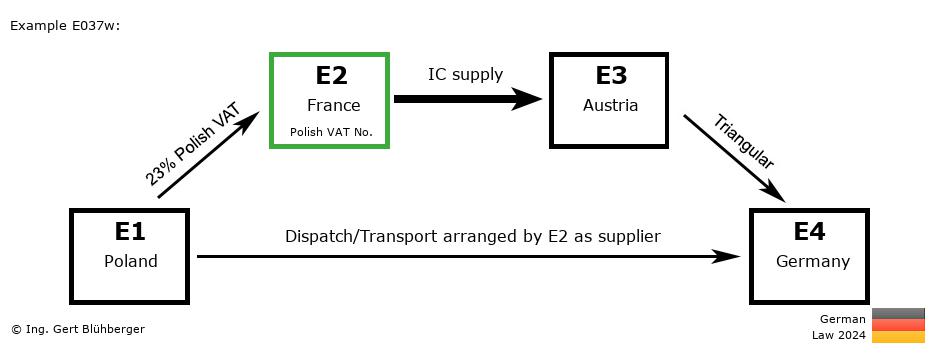

Facts:

A German entrepreneur E4 (= last purchaser) orders a machine from his Austrian supplier E3 (=2nd purchaser). The latter in turn orders the machine from the French wholesaler E2 (=1st purchaser). Since the wholesaler E2 does not have the machine in stock, he orders it from the Polish manufacturer E1 (= first supplier).

The French wholesaler E2 instructs his forwarder with the pickup of the machine from the Polish manufacturer E1 and subsequent delivery to the German entrepreneur E4. The French wholesaler E2 (=intermediary operator) acts with his Polish VAT identification number and he communicates it to the Polish manufacturer E1 in writing in the order document at the latest until the beginning of the shipment. Brief description of the triangular transaction:

- Registration obligations:

- The French entrepreneur E2 has to obtain a VAT registration in the country of departure (Poland).

- Pursuant to 25b.1. (2) UStAE, an intra-Community triangular transaction takes place in this 4-tiered chain transaction between E2, E3 and E4. No registration is required for the middle entrepreneur of a triangular transaction (in this example the Austrian entrepreneur E3) in the country of arrival.

- "Supply 1" from E1 (Poland) to E2 (France)

- Transaction without transport/dispatch assignment (§ 3 (7) UStG)

- Taxable supply in Poland (E1)

- "Supply 2" from E2 (France) to E3 (Austria)

- "Supply 3" from E3 (Austria) to E4 (Germany)

- Transaction without transport/dispatch assignment (§ 3 (7) UStG)

- Taxable supply in Germany (E4)

- Triangular transaction according to § 25b UStG

- Special features of this triangular transaction

- Since the French entrepreneur E2 acts with his Polish VAT identification number towards the Polish entrepreneur E1, the provision of the § 3 (6a) UStG (Article 36a (2) of the Directive 2006/112/EC) applies. As a result, the tax exempt supply shifts to the supply between E2 and E3 and the French entrepreneur E2 does not have to register in the destination country Germany. In addition also the Austrian entrepreneur E3 does not have to register in the destination country Germany because the simplification rules for triangular transactions, which are valid under German law, can be applied in this particular case.

- Pursuant to 25b.1. (2) UStAE, an intra-Community triangular transaction takes place in this 4-tiered chain transaction between E2, E3 and E4 as these three entrepreneurs are at the end of the supply chain (see also www.triangular-transaction.de). Due to the application of the simplification rule for triangular transactions (§ 25b UStG), the tax liability of the Austrian entrepreneur E3 is transferred to the German entrepreneur E4 (reverse charge procedure). However, it should be noted that the simplification rules for triangular transactions may not be applied in all member states in connection with 4-tiered chain transactions.

Detailed description from the perspective of the individual entrepreneurs: From the perspective of the 1st supplier E1 (from Poland): From the perspective of the 1st supplier E1 (from Poland):

Outgoing Invoice:

- Invoicing:

This supply is taxable in Poland (E1). The invoice must therefore be issued with 23 % Polish VAT, stating the own (Polish) VAT identification number.

- VAT Return:

Declaration of the sales transaction as a taxable (domestic) supply.

From the perspective of the 1st purchaser E2 (from France): From the perspective of the 1st purchaser E2 (from France):

Registration obligations:- The French entrepreneur E2 has to obtain a VAT registration in the country of departure (Poland) and act with his Polish VAT identification number towards E1 and E3. The entries listed below are consequently to be included in the Polish VAT return, ESL and Intrastat SD.

Incoming Invoice:

- VAT return (at the Polish Tax Office):

The Polish VAT contained in the incoming invoice can be deducted as input tax and must be included in the VAT return accordingly.

Outgoing Invoice:

- Invoicing:

Invoice without VAT with reference to the tax exemption (intra-Community supply) pursuant to § 4 (1)(b) UStG in conjunction with § 6a UStG (or alternatively with reference to Article 138 of the Directive 2006/112/EC) and specification of the own Polish VAT identification number as well as the (Austrian) VAT identification number of the Austrian entrepreneur E3.

No indication to the triangular transaction has to be made on this invoice!

- VAT Return (at the Polish Tax Office):

Declaration of the sales transaction as an intra-Community supply.

- EC Sales List (at the Polish Tax Office):

Declaration as (intra-Community) supply to the (Austrian) VAT identification number of the Austrian entrepreneur E3.

No labeling as a triangular transaction!

- Intrastat Supplementary Declaration (at the Polish authority):

Declaration as dispatch to Germany. Since 2022, it has also been mandatory to state the country of origin and the German VAT identification number of the German entrepreneur E4. If this is not known and cannot be determined, in exceptional cases the country code of the last purchaser (E4) may be entered in conjunction with a fictitious sequence of digits of twelve number "9" (DE999999999999). Until 2025, the country code of the invoice recipient (E3) had to be provided (AT999999999999).

From the perspective of the 2nd purchaser E3 (from Austria): From the perspective of the 2nd purchaser E3 (from Austria):

Incoming Invoice:

- VAT return:

The incoming invoice does not include VAT. The intra-Community acquisition of the middle entrepreneur in a triangular transaction is deemed to be taxed and therefore not to be included in the VAT return. It is a prerequisite that the entrepreneur E3 proves that such a triangular transaction exists and that he has met his obligation to report (by inclusion of the outgoing invoice to E4 in the ESL).

I.e. even though the entrepreneur E2 reports an intra-Community supply, the entrepreneur E3 does not have to report an intra-Community acquisition.

- Intrastat Supplementary Declaration (Intrastat SD):

In triangular transactions, the middle entrepreneur of the triangular transaction (in this example the 2nd purchaser E3) has no reporting obligation.

Outgoing Invoice:

- Invoicing:

The invoice must be issued without VAT and contain the following information: "Triangular transaction according to § 25b UStG" (or alternatively with reference to Article 141 of the Directive 2006/112/EC) and "Transfer of the tax liability pursuant to § 25b (2) UStG" (or alternatively with reference to Article 197 of the Directive 2006/112/EC) (see also 25b.1. (6) UStAE). In addition to the own (Austrian) VAT identification number, the invoice must contain the (German) VAT identification number of the German entrepreneur E4.

- VAT Return:

Due to the simplification rule of the triangular transaction, the tax liability transfers to the German entrepreneur E4. However, the value of the outgoing invoice is still to be recorded in the VAT return under "Supplies of the first purchaser in intra-Community triangular transactions according to § 25b UStG".

- EC Sales List (ESL / Recapitulative statement):

Declaration of the sales transaction to the (German) VAT identification number of the German entrepreneur E4 and labeling as a triangular transaction.

From the perspective of the last purchaser E4 (from Germany): From the perspective of the last purchaser E4 (from Germany):

Incoming Invoice:

- VAT return:

The incoming invoice contains no VAT, but the reference to the existence of a triangular transaction and the transfer of tax liability. The German entrepreneur E4 must therefore calculate the tax himself based on the German tax rates and include it on the one hand in line 47/code 69 (VAT according to § 25b (2) UStG) and on the other hand in line 38/code 66 (input VAT from intra-Community triangular transactions according to § 25b (5) UStG). This is a zero-sum game, and does not result in any payment burden.

- Intrastat Supplementary Declaration (Intrastat SD):

Declaration as arrival from Poland.

Notes to the triangular transaction:

- The above detailed descriptions from the perspective of the individual entrepreneurs represent only an indication of how the tax assessment would be if the German laws were to apply in Poland and in Austria. National deviations from the German legislation were also not taken into account in the chain transaction sketch and the brief description!

- With the BMF letter dated 25.04.2023, the Value Added Tax Application Decree (UStAE) regarding the VAT treatment of chain transactions was completely revised (incorporation of the Quick Fixes). From this date onwards, it is essential for the French entrepreneur E2 (who in this example acts as a supplier by using a Polish VAT identification number) to be able to prove, as stated in the 3.14. (10) UStAE, that he has already transmitted the VAT identification number to the Polish entrepreneur E1 before shipment (ideally in writing in the order document).

- You can find the German version in the reihengeschaeftrechner.de.

- The assessment of this chain transaction from the Austrian perspective you can find in the reihengeschaeftrechner.at.

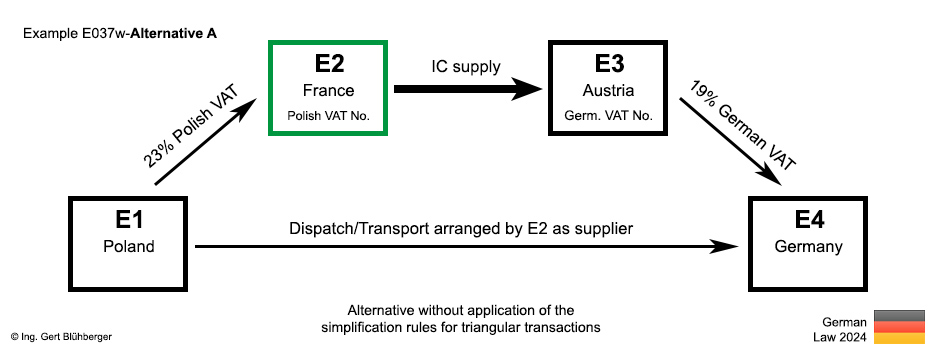

- Alternative A: If the simplification rule for triangular transactions should not or may not be applied (e.g. if the Austrian entrepreneur E3 is domiciled in Germany), then the supply from E3 to E4 is taxable in Germany (19% German VAT) and the Austrian entrepreneur E3 must register in Germany if he is not already registered. This option should also be considered if there are countries involved in the chain transaction which oppose the simplification rule for triangular transactions in the context of 4-tiered chain transactions.

|