|

|

|

|

| |

Select language / Sprache auswählen:

The triangular transaction from a German perspective

Update information Chain Transaction Calculator 2026: Whenever the use of a different VAT identification number allows a different assessment, you will find additional chain transaction sketches with the corresponding alternative examples in the evaluations of the Chain Transaction Calculator.

Depending on the chain transaction, there are up to 3 possible solutions!

Following the annual update on 1 January 2026 (including the change in the sales tax rate in Romania), a further update was carried out on 16 January 2026 to incorporate the ECJ ruling T646/24 of 3 December 2025. According to this ruling, triangular transactions can occur not only at the end but also at the beginning of a four-party chain transaction (see example 4 below).

Term Explanation:

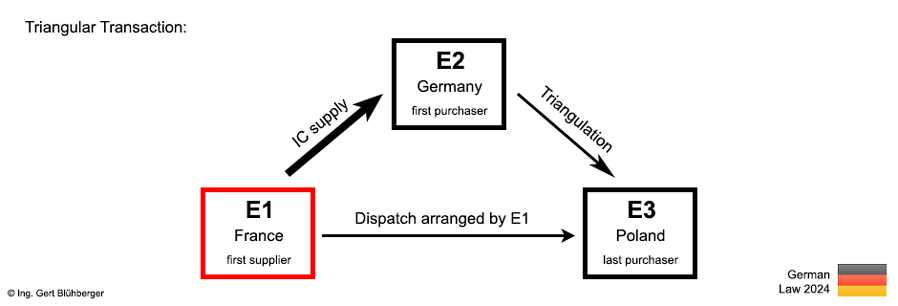

A triangular transaction is a chain transaction where a simplification rule is applied. A triangular transaction may exist where three entrepreneurs enter into sales transactions in three different Member States on one and the same commodity and this commodity passes directly from the first entrepreneur (= first supplier) to the last entrepreneur (= last purchaser).

Also, visit the chain transaction calculator. With just a few clicks, you can evaluate your particular chain and/or triangular transaction here. By clicking on the above sketch, you get directly to the triangular transaction France/Germany/Poland of the chain transaction calculator.

Facts (triangular transaction):

A Polish entrepreneur E3 (= last purchaser) orders a machine at his German merchant E2 (= first purchaser or acquirer). The latter, in turn, orders this machine from the French manufacturer E1 (= first supplier) and instructs him to dispatch the machine directly to the Polish entrepreneur E3.

Benefit of the simplification rule:

The simplification rule of § 25b UStG (German Value Added Tax Act) leads to none of the entrepreneur involved in the triangular transaction has to obtain a foreign VAT registration. Without the application of the simplification rule, the first purchaser E2 in the above example (the German merchant) would have to obtain a VAT registration in the country of arrival of the goods supplied (Poland). This would mean he would have to file monthly VAT returns.

Legal consequence of the simplification rule:

The tax liability of the first purchaser E2 transfers to the last purchaser E3 (reverse charge procedure). Thus, no taxation takes place in the Member State of the first purchaser (the entrepreneur in the middle). The intra-Community acquisition (in Germany) is deemed to be taxed and the VAT registration of the first purchaser in the country of arrival of the goods supplied (Poland) is avoided.

Without the application of the simplification rule, the first purchaser E2 would have to report an intra-Community acquisition (with right of VAT deduction) and a (taxable) domestic supply in the country of arrival of the goods supplied, as well as an additional intra-Community acquisition (without VAT deduction) in the country whose VAT identification number (also called VAT registration number) he uses in the event that he does not transact with a VAT identification number of the country of arrival (25b.1. (1) UStAE (VAT Application Decree)).

The main grounds for exclusion (from the perspective of the German legislation):

- The entrepreneurs must be registered in three different Member States. When 2 of the involved parties use the VAT identification number of the same Member State, no triangular transaction obtains.

- If the dispatch is arranged by the last entrepreneur (= last purchaser) or a pickup by him occurs, no triangular transaction takes place (but a chain transaction).

- When more than 3 entrepreneurs participate in the chain transaction, the simplification rule of the triangular transaction only applies in exceptional circumstances (see also example 7).

The detailed preconditions for a triangular transaction:

- 3 entrepreneurs have to enter into sales transactions on the same goods (§ 25b (1) (1.) UStG, 25b.1. (2) UStAE).

- The goods supplied must come directly from the first supplier to the last purchaser (§ 25b (1) (1.) UStG, 25b.1. (2) UStAE).

- The entrepreneurs involved in the triangular transaction must be registered in 3 different Member States and thus act with VAT identification numbers of 3 different Member States. The residency in a Member State does not matter, i.e. entrepreneurs from a non-EU country may also be involved (§ 25b (1) (2.) UStG, 25b.1. (3) UStAE).

- The physical movement of goods takes place between 2 Member States (from the first supplier to the last purchaser) (§ 25b (1) (3.) UStG). A previous import by the first supplier is permitted if the goods do not go directly from the third country territory to the Member State of the last purchaser (25b.1. (5) UStAE).

- The goods supplied have to be transported or dispatched by the first supplier or the first purchaser (in his capacity as purchaser). Thus, no triangular transaction occurs if the last purchaser (or the first purchaser in his capacity as supplier) collects the goods supplied at the first supplier himself or has it picked up (§ 25b (1) (4.) UStG, 25b.1. (5) UStAE).

- All involved parties except for the last purchaser must be entrepreneurs. The last purchaser may also be a legal person who is not an entrepreneur or does not acquire the object for their company § 25b (1) UStG, 25b.1. (2) UStAE).

- The first purchaser (the entrepreneur in the middle) may not be a resident in the country of arrival of the goods supplied (§ 25b (2) (2.) UStG).

- The first purchaser must act with the same VAT identification number towards the first supplier and the last purchaser and this VAT identification number must not be from a Member State where the transport or dispatch begins or ends (§ 25b (2) (2.) UStG).

- The invoice of the first purchaser to the last purchaser must contain an explicit reference to the existence of an intra-Community triangular transaction and point out the transfer of the tax liability from the first purchaser to the last purchaser (§ 25b (1) (3.) UStG, 25b.1. (8) UStAE).

- The invoice of the first purchaser to the last purchaser must also show the VAT identification number used by the first purchaser in the triangular transaction and the VAT identification number of the last purchaser (§ 25b (2) (3.) UStG, 25b.1. (8) UStAE).

- The last purchaser must be registered in the Member State of arrival of the goods supplied. This is usually the case anyway (§ 25b (2) (4.) UStG, 25b.1. (2) UStAE).

- The first purchaser must comply with his reporting obligation pursuant to § 18a (7) (4.) UStG (Recapitulative Statement also known as EC Sales List in UK). If he fails to comply with his reporting obligation, an intra-Community acquisition (without VAT deduction) is effected in the Member State of the first purchaser (§ 3d UStG).

The "technical handling" of the triangular transaction:

- The invoice of the first supplier (E1) to the first purchaser (E2) is issued without VAT and includes the words "intra-Community supply pursuant to § 4 (1)(b) UStG in conjunction with § 6a UStG" or alternatively "intra-Community supply pursuant to Art. 138 Directive on the VAT system".

- There are no special requirements for the first supplier. He deals with the business in both the VAT return (identification number 41) and in the Recapitulative Statement (EC Sales List) as if the goods were delivered to the first purchaser. There is thus no indication of a triangular transaction and also no reference to the Member State or the VAT identification number of the last purchaser.

- Since the intra-Community acquisition of the first purchaser in accordance with § 25b (3) UStG is deemed to be taxed as part of the triangular transaction, no entries in the VAT return are required for this incoming invoice.

- The invoice of the first purchaser (E2) to the last purchaser (E3) is also issued without value added tax and contains the words "Intra-Community triangular transaction according to § 25b UStG" or "Simplification rule per Art. 141 Directive on the VAT system" as well as a reference to the transfer of the tax liability to the last purchaser (25b.1. (8) UStAE).

- The first purchaser hereby conducts a supply in which the tax liability is transferred to the last purchaser. Nevertheless, the assessment bases are to be recorded in identification number 42 of the VAT return, as well as a triangular transaction in the Recapitulative Statement (EC Sales List).

- The last purchaser shows the transaction in the identification number 69 of the VAT return for the value added tax liability of the first purchaser transferred to him and, in case of entitlement to reclaim the VAT in the identification number 66 as well.

|

|

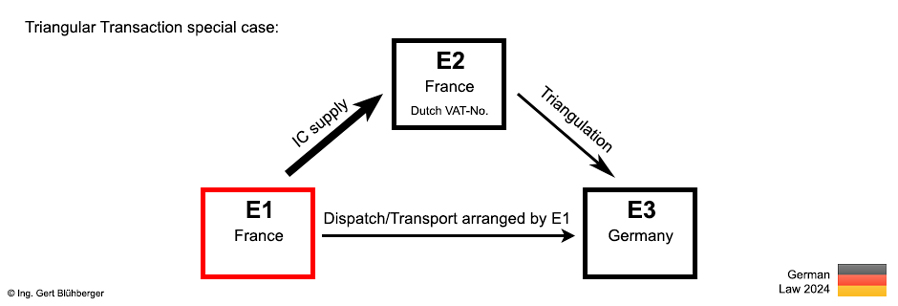

Triangular transaction special case (E1 and E2 have the same nationality):

Also, visit the chain transaction calculator. By clicking on the above sketch, you get to the appropriate example of the chain transaction calculator (www.chaintransaction-calculator.de). The example can also be evaluated for other countries here.

Facts:

A German entrepreneur E3 (=last purchaser) orders a machine from a French wholesaler E2 (=first purchaser). He, in turn orders this machine from the French manufacturer E1 (=first supplier) and instructs the latter to send the machine directly to the German entrepreneur E3. The French wholesaler E2, however, does not use his French VAT identification number but appears with a Dutch VAT identification number in this chain transaction.

Legal consequence of using three different VAT identification numbers:

- The requirement of § 25b (1) sentence 1 no. 2 UStG for the existence of an intra-Community triangular transaction is fulfilled, since the three entrepreneurs involved are each registered for VAT purposes in different Member States (France, the Netherlands, Germany) and have VAT identification numbers from different Member States. The residence of E1 and E2 in the same Member State is not relevant for the assessment (see also 25b. 1. (3) UStAE).

- The first purchaser E2 is therefore free to choose any VAT identification number with the exception of VAT identification numbers from France (country of departure) or Germany (country of destination) in order to meet the requirements for an intra-Community triangular transaction.

- The first purchaser E2 may not be a resident in the country of destination (Germany) according to § 25b (2) No. 2 UStG.

|

|

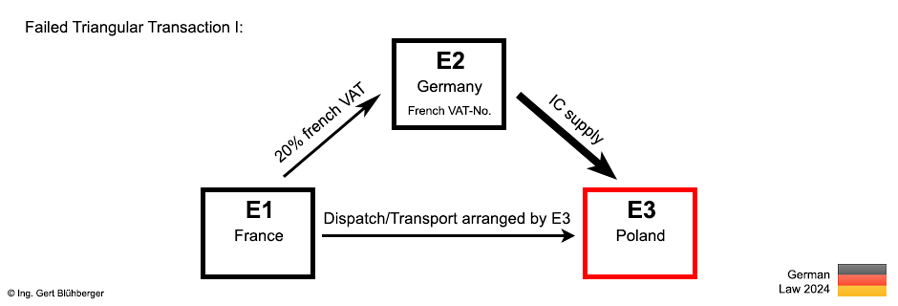

Failed triangular transaction I (when the last purchaser picks up the goods):

Also, visit the chain transaction calculator. By clicking on the above sketch, you get to the appropriate example of the chain transaction calculator (www.chaintransaction-calculator.de). The example can also be evaluated for other countries here.

Facts:

A Polish entrepreneur E3 (= last purchaser) orders a machine from a German wholesaler E2 (= first purchaser). He, in turn, orders this machine from the French manufacturer E1 (= first supplier). The last purchaser E3 has the machine picked up at the first supplier E1.

The consequences of the failed triangular transaction I:

- The supply from the French manufacturer E1 (= first supplier) to the German wholesaler E2 (= first purchaser) is a domestic supply which is per § 3 (7) (1.) UStG taxable in France.

- The supply from the German wholesaler E2 (= first purchaser) to the Polish entrepreneur E3 (= last purchaser) is an intra-Community supply which is also taxable in France according to § 3 (6) UStG but is tax exempt.

- In the example given, the German wholesaler E2 has to obtain a VAT registration in France. Consequently, the French manufacturer E1 must include the French VAT in his invoice to the German entrepreneur E2 (who now acts with a French VAT identification number). The German entrepreneur E2 has the right of deduction due to his registration in France. With the invoice from the German entrepreneur E2 (with the French VAT identification number) to the Polish entrepreneur E3, an intra-Community supply in France and at the same time an intra-Community acquisition in Poland is realised.

- In summary, it can be noted that the simplification rule of the triangular transaction does not apply if the last purchaser arranges the transport, but also in the event that the entrepreneur in the middle arranges the transport or dispatch, but acts in his capacity as a supplier. Pursuant to § 3 (6a) sentence 4 UStG the entrepreneur in the middle can either act as purchaser of the incoming supply from his vendor or as a supplier of the outgoing supply to his customer if he initiates the transport/dispatch. In this example, if the German wholesaler E2 arranges the transport and uses a French VAT identification number against the French manufacturer E1, he would act as supplier in accordance with § 3 (6a) sentence 5 UStG and the exempt supply would take place between E2 and E3 as in the example above. On the other side the supply between E1 and E2 would be taxable in France.

|

|

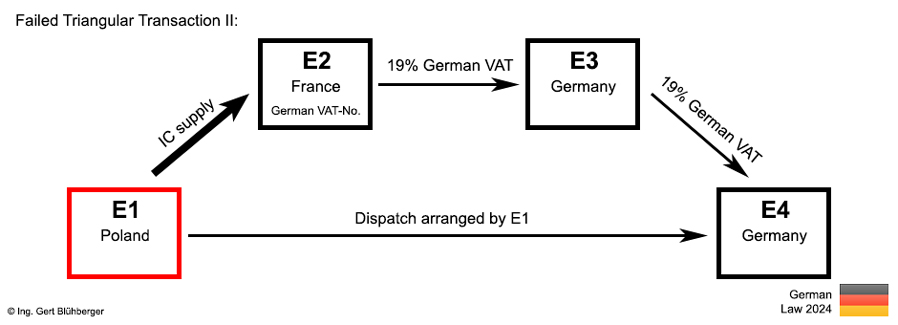

Failed triangular transaction II (when the goods are delivered to a 4th entrepreneur):

Also, visit the chain transaction calculator. By clicking on the above sketch, you get to the appropriate example of the chain transaction calculator (www.chaintransaction-calculator.de). The example can also be evaluated for other countries here.

Facts:

A German entrepreneur (E3) orders a machine from his French merchant (E2). The latter, in turn, orders this machine from the Polish manufacturer (E1). The Polish manufacturer delivers the machine as per the order to Germany, but not to the entrepreneur E3, but to E3’s customer E4, who is also established in Germany.

The consequences of the failed triangular transaction II:

- As already noted, only 3 entrepreneurs may take part in a triangular transaction (§ 25b (1) (1.) UStG) and thus it sounds at first rather unusual if a 4th entrepreneur is "mistakenly" involved at the end of the supply chain. But this is not so uncommon, as you can see in the example.

- It is often not considered that a triangular transaction is already destroyed by the 3rd (German) entrepreneur indicating a delivery address (of another entrepreneur or end customer), even if such is also located in Germany.

- Furthermore, the theory must also be clearly distinguished from the practice. If the parties involved in the chain transaction are not affiliated companies, the individual entrepreneur involved will often not have knowledge of the existence of the other entrepreneurs involved. It is therefore impossible for him to recognize that a triangular transaction may not exist due to the number of other entrepreneurs involved.

- It is even more surprising when one considers that many Member States (but not Germany) recognize triangular transactions in which the goods are not delivered to the 3rd entrepreneur in the chain, but to his customer in the same Member State. On the other hand, according to 25b.1. (2) UStAE, a triangular transaction involving 4 entrepreneurs is recognized when the three supplying entrepreneurs (of the triangular transaction) in immediate succession are at the end of the supply chain.

- In the example described, the French entrepreneur E2 would be obligated to register in the Member State of arrival (Germany) and act with his German VAT identification number. If he fails to do so and acts with his French VAT identification number, a so-called double acquisition takes place. I.e. he realizes an intra-Community acquisition in Germany and simultaneously an intra-Community acquisition in France due to acting with the French VAT identification number. He is obliged to pay the VAT (acquisition tax) in both Member States (and thus twice), but is not entitled to reclaim this tax due as input VAT in France. This double acquisition ceases to apply only when he proves the taxation of the intra-Community acquisition in Germany (§ 3d UStG).

Failed or not failed?

Assessment of this (possibly not failed) triangular transaction based on the latest European case law (ECJ judgment T464/24 of December 3, 2025):

- In the context of these proceedings, the following question, among others, was referred to the court for a preliminary ruling:

Must Article 141(c) of the VAT Directive, on which, in accordance with Articles 42 and 197 thereof, the non-application of the first paragraph of Article 41 depends, be interpreted as meaning that the condition laid down in that provision is satisfied when the goods in question are supplied (that is, made available in terms of possession or ownership) under a single transport operation to the customer of the person acquiring the goods (and not to the third person in the transaction chain), which is registered for VAT purposes in the same Member State as the third person in the transaction chain?

- The General Court (Chamber giving preliminary rulings) hereby rules:

Article 141(c) of Council Directive 2006/112/EC of 28 November 2006 on the common system of value added tax, as amended by Council Directive 2010/45/EU of 13 July 2010, must be interpreted as meaning that the fact that the goods supplied in the context of a triangular transaction are not physically transported to the person for whom the subsequent supply is carried out, but to his or her customer, to whom that person resells them and who is identified for value added tax (VAT) purposes in the same Member State as the reseller, does not preclude the condition laid down in that provision from being regarded as satisfied.

- Conclusion: The application of the simplification rules for triangular transactions is therefore permissible in a chain transaction with 4 entrepreneurs even if the goods are not delivered to the third entrepreneur (E3) but to his customer (E4). The only prerequisite mentioned in the ruling is that E3 and E4 must be registered for VAT purposes in the same member state. This requirement is fulfilled in the example shown above. Accordingly, the French entrepreneur E2 could use his own (French) VAT ID number and apply the simplification rules for triangular transactions in his invoice to the German entrepreneur E3. This would mean that he would not have to register in Germany and the VAT liability would be transferred to the German entrepreneur E3.

- What is the problem at the moment?

Section 25b.1. (2) of the German VAT Implementation Regulation (UStAE) recognizes a triangular transaction within a four-party chain transaction, but only if the three entrepreneurs (in the triangular transaction) supplying directly one after the other are at the end of the supply chain (and thus a triangular transaction between entrepreneurs U2, U3, and U4 is represented).

This contradicts the above ruling of the European Court of Justice, which recognizes a triangular transaction within a four-party chain transaction in which the three entrepreneurs (in the triangular transaction) supplying directly one after the other are at the beginning of the supply chain (and thus a triangular transaction between entrepreneurs U1, U2, and U3 is represented). The ruling therefore denies the legal basis for the view expressed in section 25b.1. (2) UStAE. One can therefore only hope that the new European case law will be taken into account in the VAT application decree in a timely manner.

|

|

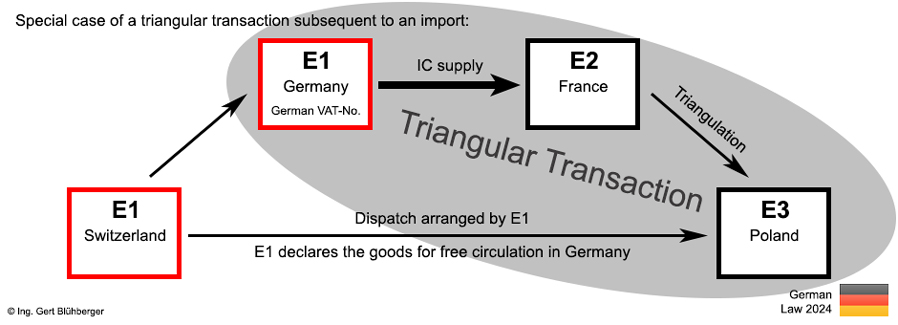

Special case of a triangular transaction subsequent to an import:

Facts:

A Polish entrepreneur (E3) orders a machine from his French merchant (E2). The latter, in turn, orders this machine from his Swiss manufacturer (E1). The manufacturer delivers the machine to Poland as per the order. The Swiss manufacturer (E1) declares the goods for free circulation in Germany and delivers "duty and taxes paid".

Legal consequence and handling of the transaction having a preceding import from a non-EU country:

- The condition that 3 entrepreneurs must be involved in the triangular transaction where they must be registered in 3 different Member States is met in the example shown. Since the residence in a Member State does not matter, the fact that the 1st entrepreneur resides in a non-EU country is not detrimental.

- The place of supply is shifted to the domestic country (Germany) pursuant to § 3 (8) UStG. From a tax perspective, the Swiss entrepreneur (E1) must register in Germany and thus has a German VAT identification number.

- The triangular transaction that now follows the import, starts in Germany because the Swiss manufacturer (E1) acts with his German VAT identification number and continues through France (E2) to Poland (E3).

- The invoice of the Swiss manufacturer (E1) to the French merchant (E2) is issued without value added tax and contains the words "intra-Community supply according to § 4 (1)(b) UStG in conjunction with § 6a UStG". The invoice must contain both the German VAT identification number of the Swiss supplier (E1) as well as the VAT identification number of the French entrepreneur E2.

- The invoice from the French merchant (E2) to the Polish customer (E3) is also issued without value added tax and includes the words "Intra-Community triangular transaction according to § 25b UStG" and transfer of tax liability. The invoice must contain both the VAT identification number of the French entrepreneur E2 and the VAT identification number of the Polish entrepreneur E3. (§ 25b (1) (3.) UStG, 25b.1. (8) UStAE). Furthermore, the entrepreneur E2 must meet his reporting obligation according to § 18a (7) (4.) UStG (EC-Sales-List / Recapitulative Statement).

- As a legal consequence of the triangular transaction and by taking advantage of the simplification rule, the tax liability of the French entrepreneur E2 transfers to the Polish entrepreneur E3 (reverse charge procedure). No taxation thus occurs in France (the intra-Community acquisition is deemed to be taxed).

|

|

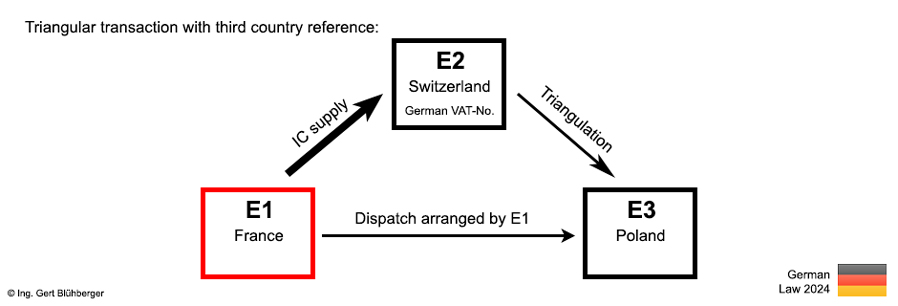

Triangular transaction with third country reference (the first purchaser is based in the non-EU country):

Facts:

A Polish entrepreneur (E3) orders a machine from a Swiss merchant (E2). The latter, in turn, orders this machine from the French manufacturer (E1), who delivers the machine in accordance with the contract directly to the Polish entrepreneur (E3). The Swiss merchant (E2) acts with his German VAT identification number.

Legal consequence of the triangular transaction with third party country reference:

- The condition that 3 entrepreneurs must be involved in the triangular transaction where they must be registered in 3 different Member States is met in the example shown. Since the residence in a Member State does not matter, the fact that the entrepreneur in the middle (E2) resides in a non-EU country is not detrimental.

- From a tax law perspective, the Swiss entrepreneur (E2) has to obtain a VAT registration in Germany (or in another EU Member State) and thus has a German VAT identification number. He therefore integrates himself into the triangular transaction like an entrepreneur of a Member State.

- As a legal consequence of the triangular transaction and by taking advantage of the simplification rule, the tax liability of the first purchaser E2 transfers to the last purchaser E3 (reverse charge procedure). Thus, no taxation takes place in the Member State of the first purchaser E2 (i.e. the intra-Community acquisition is deemed to be taxed).

- According to the ECJ judgment, the rule that for the entrepreneur in the middle of a triangular transaction it does not depend on the residence in a member state, but only on the fact that he acts with a VAT identification number that is not issued from the country of departure and also not from the country of destination, can even be applied if the entrepreneur in the middle has the same nationality as the first supplier. In the above example, the entrepreneur E2 could be a Frenchman like E1 and, for example, act with a German VAT identification number. This would not be harmful to the triangular transaction.

|

|

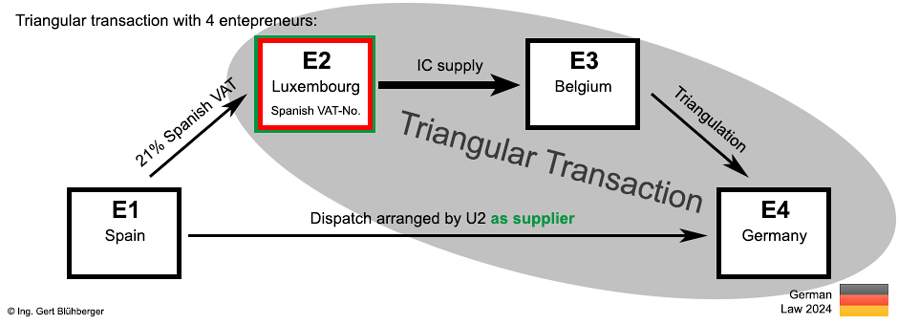

Triangular transaction with 4 entrepreneurs:

Facts:

A German entrepreneur (E4) orders tool parts from his Belgian supplier (E3). The Belgian entrepreneur (E3) does not have these in stock and hence orders them from his wholesaler (E2) in Luxembourg. Since the wholesaler E2 does not have the tool parts in stock, either, he orders these from the Spanish manufacturer (E1). The wholesaler E2 instructs his freight forwarder with the pick-up of the tool parts in Spain and subsequent delivery to the German entrepreneur E4. The wholesaler E2 acts with his Spanish VAT identification number.

Legal consequences of the triangular transaction with 4 entrepreneurs:

- Pursuant to § 25b (1) UStG, an intra-Community triangular transaction only obtains when 3 entrepreneurs conclude sales transactions on the same item and this item passes directly from the first supplier to the last purchaser. Under this provision of the German Value Added Tax Act, the simplification rule of the triangular transaction should not apply in the above example.

- Nevertheless, according to 25b.1. (2) of the VAT application decree, an intra-Community triangular transaction can take place between three supplying entrepreneurs in immediate succession in the case of chain transactions with more than three participants, if the three entrepreneurs are at the end of the supply chain. According to the example shown in the VAT application decree, the triangular transaction is split off the remaining supplies. For the application of the simplification rule, it is only necessary that the intra-Community supply is assigned to the first sales transaction within the triangular transaction (E2 to E3). In the above example, this is achieved by the fact that the second entrepreneur (and thus the first entrepreneur within the triangular transaction) acts in his capacity as a supplier (see also § 3 (6a) sentences 4 and 5).

- As a legal consequence, the triangular transaction to which the simplification rule applies takes place between the entrepreneurs E2, E3 and E4. The tax liability of the Belgian entrepreneur E3 is transferred to the last purchaser E4 (reverse charge procedure). Consequently, no taxation takes place in the Member State of entrepreneur E3 (the intra-Community acquisition is deemed to be taxed) and the VAT registration of the Belgian entrepreneur in the country of arrival (Germany) is avoided.

- Pursuant to § 3 (6) UStG, Spain is the place of supply of the transaction between E2 and E3. The entrepreneur E2 from Luxembourg must therefore register in Spain and act with his Spanish VAT identification number. However, the transaction is tax exempt as intra-Community supply.

- The first transaction (E1 to E2) is also taxable in Spain (§ 3 (7) (1.) UStG). The Spanish entrepreneur E1 needs to include the Spanish value added tax in his invoice to the entrepreneur E2 (who now acts with a Spanish VAT identification number). The entrepreneur E2 from Luxembourg has the right of deduction due to his registration in Spain.

Notes on the triangular transactions with 4 entrepreneurs pursuant to 25b.1. (2) UStAE:

- The Directive on the VAT system contains no indication as to whether a triangular transaction may be located within a (more than 3-member) chain transaction. Accordingly, the rules on this differ in the individual member states. The application of the German regulation may thus, subject to the laws of the other Member States concerned, well lead to a double acquisition (i.e. additional intra-Community acquisition without right of deduction) in those Member States.

|

|

Failed triangular transaction (incorrect invoice):

ECJ Decision of 08.12.2022 - Rs C-247/21 Luxury Trust Automobil GmbH:

It should already be known that in a triangular transaction the 1st purchaser must not forget 2 essential invoice features in his invoice to the last purchaser:

- Reference to an intra-Community triangular transaction

- Reference to the transfer of the tax liability to the recipient of the service

An interesting question in this context is what happens when the reference to the transfer of the tax liability is missing in an invoice. Actually, the last purchaser should already recognise that he owes the tax for the first purchaser by referring to the existence of a triangular transaction.

Unfortunately, the ECJ sees things differently! In the decision of 08.12.2022, it clarifies that this reference is mandatory and that the ultimate purchaser in the context of a triangular transaction has not been effectively designated as the debtor for VAT if the invoice issued by the intermediate purchaser does not contain the indication "liability of the recipient for VAT" pursuant to Art. 226 No. 11a of the Directive. In such a case, therefore, the simplification rules for triangular transactions cannot be applied and there is accordingly a chain transaction.

Legal consequence if a triangular transaction is disallowed (double acquisition):

- The 1st purchaser in a triangular transaction, as the recipient of the supply with transport/dispatch assignment, has made an intra-Community acquisition in the Member State of destination. This acquisition is tax-exempt in the case of a triangular transaction. However, if the triangular transaction is disallowed due to the incorrect invoice, then this tax exemption no longer applies!

- In addition, the first purchaser in the context of a triangular transaction has made an intra-Community acquisition in the VAT state (i.e. in the member state whose VAT number he used). This so-called double acquisition is deemed to be taxed in the context of a triangular transaction if the 1st purchaser fulfils his obligations. If the triangular transaction is disallowed due to the incorrect invoice, then this double acquisition remains. This means that the 1st purchaser must pay the acquisition tax, but may not claim this amount as input tax at the same time as usual!

Can such a mistake be remedied?

In the same ruling of 08.12.2022, the ECJ clarifies that the omission of the required information "tax liability of the recipient of the service" on an invoice cannot be corrected later by adding a reference to it. This is justified by the fact that there can be no question of correcting the invoice if a prerequisite for the application of the derogation applicable to triangular transactions is missing. This is the first issuance of the required invoice, which cannot have retroactive effect.

|

| |

In addition to the above notes, see excerpts of the relevant legal provisions relating to triangular transactions under the following links:

Note to the links to laws, guidelines and regulations: With the exception of the Directive of the VAT system, these are in German (also in the full version).

Please note the Terms of Use and the Disclaimer of Liability.

|

| |

| |

|

Ing. Gert Bluehberger

Arbeiterstrandbadstrasse 21

1210 Vienna

Austria |

Phone.:

Fax:

Email:

|

+43 660 / 666 00 26

+43 1 263 00 51

office 1 @ bilanzbuchhaltung-wien.at

(without space)

|

|