Facts:

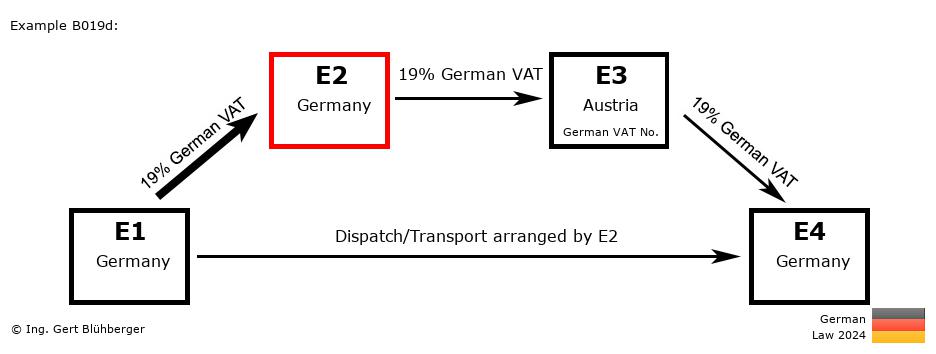

A German entrepreneur E4 (= last purchaser) orders a machine from his Austrian supplier E3 (=2nd purchaser). The latter in turn orders the machine from the German wholesaler E2 (=1st purchaser). Since the wholesaler E2 does not have the machine in stock, he orders it from the German manufacturer E1 (= first supplier).

The German wholesaler E2 instructs his forwarder with the pickup of the machine from the German manufacturer E1 and subsequent delivery to the German entrepreneur E4. Brief description of the chain transaction:

- Registration obligations:

- The Austrian entrepreneur E3 has to obtain a VAT registration in the destination country Germany.

- "Supply 1" from E1 (Germany) to E2 (Germany)

- "Supply 2" from E2 (Germany) to E3 (Austria)

- Transaction without transport/dispatch assignment (§ 3 (7) UStG)

- Taxable supply in Germany (E4)

- "Supply 3" from E3 (Austria) to E4 (Germany)

- Transaction without transport/dispatch assignment (§ 3 (7) UStG)

- Taxable supply in Germany (E4)

- Special features of this chain transaction

- Since § 3 (6a) sentence 5 UStG refers only to chain transactions where the goods pass from one Member State to another, in this example, the dispatch/transport is assigned to the supply from E1 to E2, although the entrepreneur E2 appears with a VAT identification number of the country of departure. If, on the other hand, entrepreneur E2 proves that he transports the goods in his capacity as supplier (§ 3 (6a) sentence 4 - 2nd half sentence UStG), the dispatch/transport would be assigned to the supply from E2 to E3. However, since in the present example all supplies are taxable in Germany, this assignment has no particular relevance.

- Since the goods do not leave the country, there is no tax-exempt supply in this chain transaction.

Detailed description from the perspective of the individual entrepreneurs: From the perspective of the 1st supplier E1 (from Germany): From the perspective of the 1st supplier E1 (from Germany):

Outgoing Invoice:

- Invoicing:

This supply is taxable in Germany (E1). The invoice must therefore be issued with 19 % German VAT, stating the own (German) VAT identification number.

- VAT Return:

Declaration of the sales transaction in line 13/code 81 as taxable (domestic) supply.

From the perspective of the 1st purchaser E2 (from Germany):Incoming Invoice:

- VAT return:

The German VAT contained in the incoming invoice can be deducted as input tax and must be included in the VAT return in line 38/code 66.

Outgoing Invoice:

- Invoicing:

This supply is taxable in Germany (E4). The invoice must therefore be issued with 19 % German VAT and specification of the own (German) VAT identification number.

- VAT Return:

Declaration of the sales transaction in line 13/code 81 as taxable (domestic) supply.

From the perspective of the 2nd purchaser E3 (from Austria): From the perspective of the 2nd purchaser E3 (from Austria):

Registration obligations:- The Austrian entrepreneur E3 has to obtain a VAT registration in the destination country Germany and act with his German VAT identification number towards E2 and E4. The entries listed below must therefore be included in the German VAT return.

Incoming Invoice:

- VAT return (at the German Tax Office):

The German VAT contained in the incoming invoice can be deducted as input tax and must be included in the VAT return in line 38/code 66.

Outgoing Invoice:

- Invoicing:

This supply is taxable in Germany (E4). The invoice must therefore be issued with 19 % German VAT and specification of the own German VAT identification number.

- VAT Return (at the German Tax Office):

Declaration of the sales transaction as a taxable (domestic) supply in line 13/code 81 and payment of the VAT from this supply to the German Tax Office.

From the perspective of the last purchaser E4 (from Germany):

Incoming Invoice:

- VAT return:

The German VAT contained in the incoming invoice can be deducted as input tax and is to be included in the VAT return in line 38/code 66.

Notes to the chain transaction:

Please note the Terms of Use and the Disclaimer of Liability. |