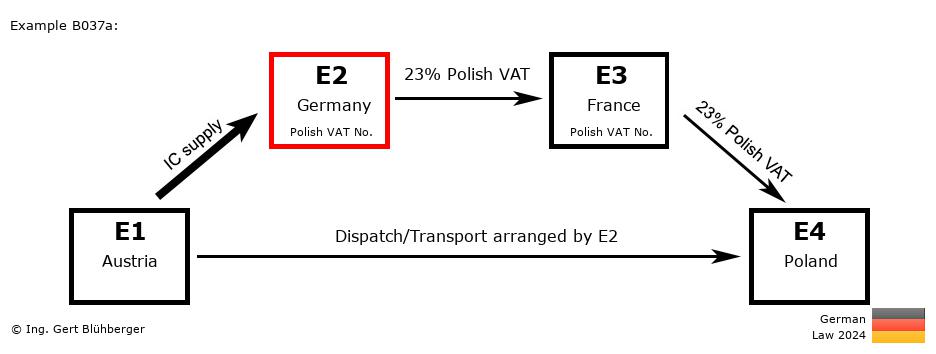

Facts:

A Polish entrepreneur E4 (= last purchaser) orders a machine from his French supplier E3 (=2nd purchaser). The latter in turn orders the machine from the German wholesaler E2 (=1st purchaser). Since the wholesaler E2 does not have the machine in stock, he orders it from the Austrian manufacturer E1 (= first supplier).

The German wholesaler E2 instructs his forwarder with the pickup of the machine from the Austrian manufacturer E1 and subsequent delivery to the Polish entrepreneur E4. Brief description of the chain transaction:

- Registration obligations:

- The German entrepreneur E2 has to obtain a VAT registration in the destination country Poland.

- The French entrepreneur E3 as well has to obtain a VAT registration in the destination country Poland.

- "Supply 1" from E1 (Austria) to E2 (Germany)

- "Supply 2" from E2 (Germany) to E3 (France)

- Transaction without transport/dispatch assignment (§ 3 (7) UStG)

- Taxable supply in Poland (E4)

- "Supply 3" from E3 (France) to E4 (Poland)

- Transaction without transport/dispatch assignment (§ 3 (7) UStG)

- Taxable supply in Poland (E4)

Detailed description from the perspective of the individual entrepreneurs: From the perspective of the 1st supplier E1 (from Austria): From the perspective of the 1st supplier E1 (from Austria):

Outgoing Invoice:

- Invoicing:

Invoice without VAT with reference to the tax exemption (intra-Community supply) pursuant to § 4 (1)(b) UStG in conjunction with § 6a UStG (or alternatively with reference to Article 138 of the Directive 2006/112/EC) and specification of the own (Austrian) VAT identification number as well as the Polish VAT identification number of the German entrepreneur E2.

- VAT Return:

Declaration of the sales transaction as an intra-Community supply.

- EC Sales List (ESL / Recapitulative statement):

Declaration as (intra-Community) supply to the Polish VAT identification number of the German entrepreneur E2.

- Intrastat Supplementary Declaration (Intrastat SD):

Declaration as dispatch to Poland. Since 2022, the country of origin and the Polish VAT identification number of the German entrepreneur E2 must also be reported.

From the perspective of the 1st purchaser E2 (from Germany): From the perspective of the 1st purchaser E2 (from Germany):

Registration obligations:- The German entrepreneur E2 has to obtain a VAT registration in the destination country Poland and act with his Polish VAT identification number towards E1 and E3. The entries listed below are consequently to be included in the Polish VAT return and Intrastat SD.

Incoming Invoice:

- VAT return (at the Polish Tax Office):

The incoming invoice contains no VAT and is to be included as an intra-Community acquisition in the VAT return. Therefore, on the one hand, the VAT (acquisition tax) must be paid and, on the other hand, it can be treated as input tax on the same return.

- Intrastat Supplementary Declaration (at the Polish authority):

Declaration as arrival from Austria.

Outgoing Invoice:

- Invoicing:

This supply is taxable in Poland (E4). The invoice must therefore be issued with 23 % Polish VAT and specification of the own Polish VAT identification number.

- VAT Return (at the Polish Tax Office):

Declaration of the sales transaction as a taxable (domestic) supply and payment of the VAT from this supply to the Polish Tax Office.

From the perspective of the 2nd purchaser E3 (from France): From the perspective of the 2nd purchaser E3 (from France):

Registration obligations:- The French entrepreneur E3 has to obtain a VAT registration in the destination country Poland and act with his Polish VAT identification number towards E2 and E4. The entries listed below must therefore be included in the Polish VAT return.

Incoming Invoice:

- VAT return (at the Polish Tax Office):

The Polish VAT contained in the incoming invoice can be deducted as input tax and must be included in the VAT return accordingly.

Outgoing Invoice:

- Invoicing:

This supply is taxable in Poland (E4). The invoice must therefore be issued with 23 % Polish VAT and specification of the own Polish VAT identification number.

- VAT Return (at the Polish Tax Office):

Declaration of the sales transaction as a taxable (domestic) supply and payment of the VAT from this supply to the Polish Tax Office.

From the perspective of the last purchaser E4 (from Poland): From the perspective of the last purchaser E4 (from Poland):

Incoming Invoice:

- VAT return:

The Polish VAT contained in the incoming invoice can be deducted as input tax and must be included in the VAT return accordingly.

Notes to the chain transaction:

- CAUTION: If the German entrepreneur E2 does not operate with a Polish VAT identification number but with his own German VAT identification number, for example, an additional intra-Community acquisition is triggered in the country of the used VAT identification number without entitlement to deduct VAT (§ 3d Sentence 2 UStG). This means that the entrepreneur E2 must pay VAT (acquisition tax) in Germany without entitlement to reclaim this VAT as input VAT. See also 3.14. (13) example 1 UStAE. Excluded from this is the solution shown in the alternative.

- The above detailed descriptions from the perspective of the individual entrepreneurs represent only an indication of how the tax assessment would be if the German laws were to apply in Austria and in Poland. National deviations from the German legislation were also not taken into account in the chain transaction sketch and the brief description!

- In addition to the entries in the VAT return as stated above, the German entrepreneur E2 must record in the German VAT return in line 36/code 45 supplies that are not taxable in Germany whose place of supply is outside Germany and which would be taxable if they would be carried out within the country.

- You can find the German version in the reihengeschaeftrechner.de.

- The assessment of this chain transaction from the Austrian perspective you can find in the reihengeschaeftrechner.at.

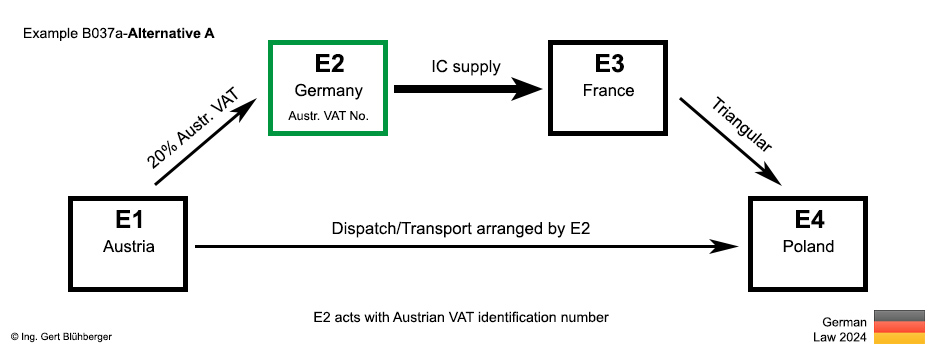

- Alternative A: If the German entrepreneur E2 acts with an Austrian VAT identification number towards the Austrian entrepreneur E1, the tax exempt supply shifts to the supply between E2 and E3. This would make the simplification rules of the triangular transaction applicable and the tax liability of the French entrepreneur E3 is transferred to the Polish entrepreneur E4. However, the supply from E1 to E2 is then taxable in Austria (20% Austr. VAT). The detailed description of this variant can be found by clicking on the "E2 as supplier"-button in the selection screen.

|