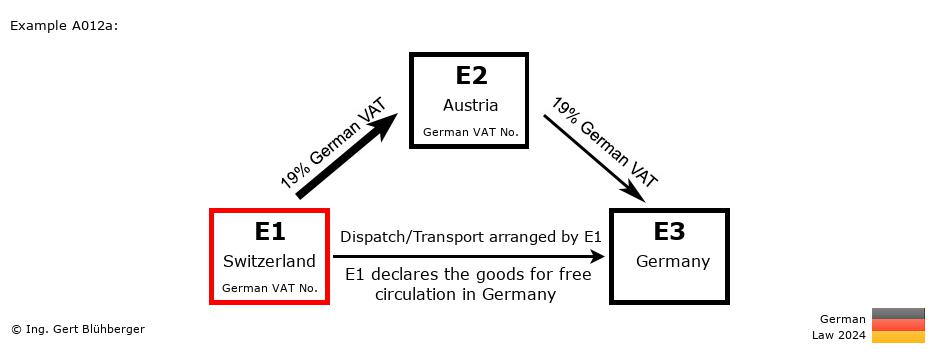

Facts:

A German entrepreneur E3 (= last purchaser) orders a machine at his Austrian supplier E2 (=1st purchaser). Since the supplier E2 does not have the machine in stock, he orders it from the Swiss wholesaler E1 (=first supplier) and instructs him to dispatch the machine directly to the German entrepreneur E3. The Swiss wholesaler E1 declares the goods for free circulation in Germany, delivers them "duty and tax paid" and is therefore liable to pay the import VAT. Brief description of the chain transaction:

- Registration obligations:

- The Swiss entrepreneur E1 has to obtain a VAT registration in the country in which the goods are declared for free circulation (Germany).

- The Austrian entrepreneur E2 has to obtain a VAT registration in the destination country Germany.

- "Supply 1" from E1 (Switzerland) to E2 (Austria)

- Assignment of transport or dispatch according to § 3 (6a) sentence 2 UStG

- Taxable supply in Germany

- "Supply 2" from E2 (Austria) to E3 (Germany)

- Transaction without transport/dispatch assignment (§ 3 (7) UStG)

- Taxable supply in Germany (E3)

- Import value added tax:

- Since the Swiss entrepreneur E1 has the right to dispose of the goods when crossing the border, he is entitled to reclaim the import VAT as input VAT.

- If entrepreneur E1 commissioned the transport but does not deliver "duty and tax paid" and the declaration for free circulation is made for entrepreneur E2 (or another entrepreneur), no relocation of the place of supply pursuant to § 3 (8) UStG takes place. The entrepreneur E1 would not have to register in the destination country Germany anymore.

If the declaration for free circulation is done by a subsequent entrepreneur, § 4 No. 4b UStG applies and once all conditions are met, the supplies before the import are tax exempt. The declarant is furthermore entitled to reclaim the import VAT as input VAT (see also 3.14. (16) example 1 UStAE). This applies in any case if the goods were previously in a bonded warehouse. If, on the other hand, the goods were declared for free circulation already when they crossed the border, please pay attention to example 8 at www.chain-transaction.de.

- Special feature of this chain transaction

- Since the supplier E1 undertakes the declaration for free circulation (and is therefore liable to pay the import VAT), a relocation of the place of supply according to § 3 (8) UStG to Germany takes place. As a result, the supply between E1 and E2 is taxable in Germany (19% German VAT) and the Swiss entrepreneur E1 has to register in Germany.

Detailed description from the perspective of the individual entrepreneurs: From the perspective of the 1st supplier E1 (from Switzerland): From the perspective of the 1st supplier E1 (from Switzerland):

Registration obligations:- The Swiss entrepreneur E1 has to obtain a VAT registration in the country in which the goods are declared for free circulation (Germany) and act with his German VAT identification number towards E2.

Outgoing Invoice:

- Invoicing:

This supply is taxable in Germany due to the relocation of the place of supply to Germany pursuant to § 3 (8) UStG. The invoice must therefore be issued with 19 % German VAT and stating the own German VAT identification number.

- VAT Returns:

a) at the Swiss Tax Office: A declaration in the VAT Return is governed by the statutory provisions of the third country.

b) at the German Tax Office: Declaration of the sales transaction in line 13/code 81 as a taxable (domestic) supply and payment of the VAT from this supply to the German Tax Office.

In order to reclaim the import VAT as input VAT, the import VAT is to be included in the VAT Return in line 40/code 62 (Resulting Import VAT).

From the perspective of the 1st purchaser E2 (from Austria): From the perspective of the 1st purchaser E2 (from Austria):

Registration obligations:- The Austrian entrepreneur E2 has to obtain a VAT registration in the destination country Germany and act with his German VAT identification number towards E1 and E3. The entries listed below must therefore be included in the German VAT return.

Incoming Invoice:

- VAT return (at the German Tax Office):

The German VAT contained in the incoming invoice can be deducted as input tax and must be included in the VAT return in line 38/code 66.

Outgoing Invoice:

- Invoicing:

This supply is taxable in Germany (E3). The invoice must therefore be issued with 19 % German VAT and specification of the own German VAT identification number.

- VAT Return (at the German Tax Office):

Declaration of the sales transaction as a taxable (domestic) supply in line 13/code 81 and payment of the VAT from this supply to the German Tax Office.

From the perspective of the last purchaser E3 (from Germany): From the perspective of the last purchaser E3 (from Germany):

Incoming Invoice:

- VAT return:

The German VAT contained in the incoming invoice can be deducted as input tax and must be included in the VAT return in line 38/code 66.

Notes to the chain transaction:

Please note the Terms of Use and the Disclaimer of Liability. |